All indices across different markets were range bound for most of September before breaking out to finish the month at or close to month’s high.

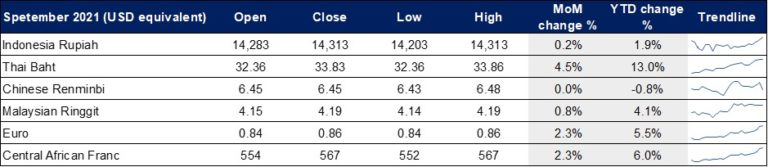

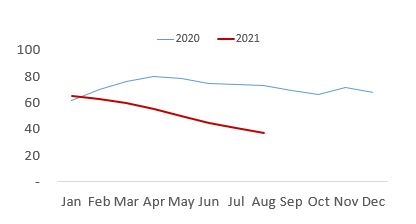

Overview of forex trends for September 2021

Source: Bloomberg

In general, USD appreciated against all listed currencies except for Chinese RMB in September as rising U.S. treasury yield, caused by Fed’s policy tightening outlook, sparked fund inflows back into USD.

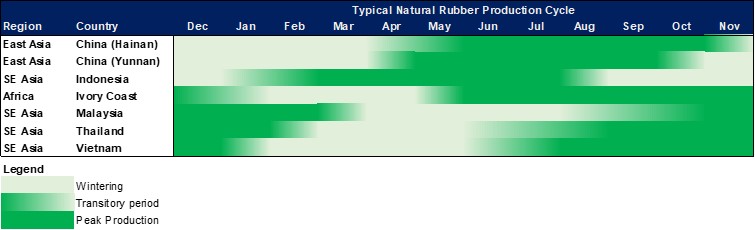

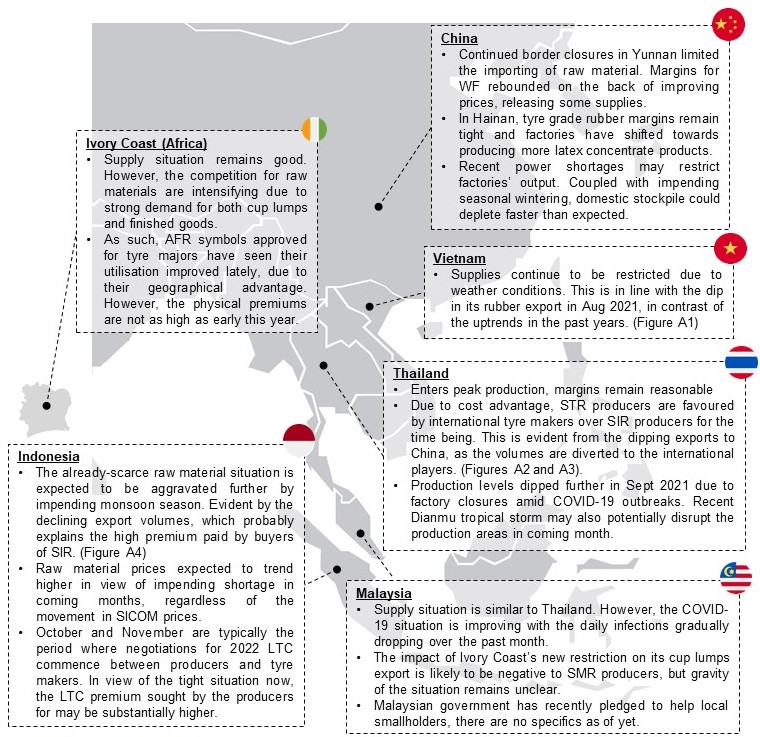

Overview of supply situation by key origins

Overview of demand situation

International

Demand level continues to be healthy, despite the recent chip shortage situation experienced by automakers.

It has also been observed the tyre makers have pivoted to ship the dry rubber to destinations through breakbulk shipments, rather than the conventional containers. This should alleviate the inventory shortage situation at year end.

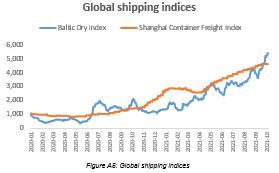

Freight rates remains high, but the rate of increase slowed during September. (Figure A5)

China

The capacity utilisation of the PRC-based tyre factories is stable from previous months, in absence of any obvious stimulating factor. However, as aforementioned, the widespread power outage in key industrial and commercial provinces would be a near-term risk factor.

Despite the stable operating rates in factories and the logistical congestion situation, China is exporting more tyres than ever, an indication of the strong automotive demand globally.

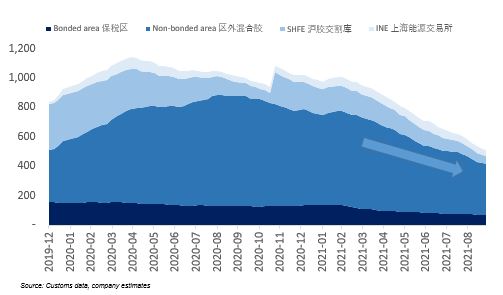

Hence, China is drawing down from inventories to fulfil the surging demand, which caused overall stocks level to continue dropping. They are now running on much lower stock reserves – equivalent to one month of domestic consumption as of now, more than halved from year-ago period. It is also uncertain as to when China will restock its strategic reserve.

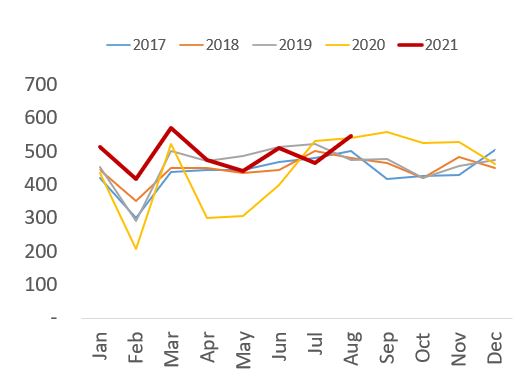

Tyre exports from China (in kmT)

NR stocks in China over average daily consumption (expressed in days)

Estimated natural rubber stock level in kmT

Concluding thoughts

On the supply side, there are conflicting factors at play: Despite the origins entering seasonal peak production, but the heavy rain as a result of monsoon and typhoons may limit the potential upside. Raw material scarcity may remain a major theme for the supply in coming months.

However, from a demand point of view, the international automakers and tyre makers have been procuring tyres and rubber rather aggressively. Meanwhile, the PRC domestic tyre makers’ utilisation rates appear to be weakening given the recent revelations. As the restocking has yet to take place, it may indicate that the rubber sources that has been historically destined towards China (most prominently being Thailand) may have been snapped up by the international tyre makers. Assuming that there are no new sources coming online, Chinese tyre makers may face supply pressure when they decide to re-stock.

Disclaimers

This report has been prepared by Halcyon Agri Corporation Limited (“Company”) for informational purposes, and may contain projections and forward-looking statements that reflect the Company’s current views with respect to future events and financial performance. These views are based on current assumptions which are subject to various risks and which may change over time. No assurance can be given that future events will occur, that projections will be achieved, or that the Company’s assumptions are correct.

The information is current only as of the date of this report and shall not, under any circumstances, create any implication that the information is correct as of any time subsequent to the date of this report or that there has been no change in the financial condition or affairs of the Company since such date. Opinions expressed in this report reflect the judgement of the Company as of the date of this report and may be subject to change. This report may be updated from time to time and there is no undertaking by the Company to post any such amendments or supplements on this report.

The Company will not be responsible for any consequences resulting from the use of this report as well as the reliance upon any opinion or statement contained within this report or for any omission.

Information in this report has been extracted and/or reproduced from published or otherwise publicly available sources, and the sole responsibility of the Company has been to ensure through reasonable enquiries that such information is accurately extracted from such sources and reflected or, as the case may be, reproduced in its proper form and context. The Company takes no responsibility whatsoever for the accuracy and/or correctness of such information.