2018 Rubber Commentary by Chief Economist George Sulkowski

2018 may well prove to have been a seminal year for both the rubber industry as a whole and the rubber market in particular. It’s questionable whether globalisation has done the industry any favours as an over 100-year old disease, known generically as South American Leaf Blight (SALB), today has many ways of reaching beyond its original borders. Questionable? Only because it may in fact have ‘helped’ so far by limiting output in a time of surplus – but that’s short-termism.

As Malaysia’s plantation dominance and domestic output faded over the last decade of the 1900s, its processing capacity didn’t, the rise of raw material import, initially from Africa to support latent capacity, being a direct consequence. SALB monitoring stations in strategic positions across the tropics are no defense against disease ‘tourism’ as spores can travel safely containerised across the seas, or above them, possibly even as first-class passengers, airliners crisscrossing the globe daily, precautions limited or non-existent. This is not to say that the fungus currently affecting parts of South East Asia came from Africa, but it illustrates the ease in which other more potent diseases can transfer across continents. SALB has been the rubber industry’s worst nightmare for most of its history and while its current incidence in South East Asia is still far from having reached crisis proportions, being blasé about it is certainly not an option.

SALB apart, and with rubber statistics being nominal at best, the latter part of the year in review saw a general decline in the price discovery influence of the industry’s various paper markets, dominated as they have been by negative sentiments – mostly engendered outside of rubber’s orbit – and by the growing incidence of algorithm trading and speculative activity that take no account of cost or consequence. It seems that rubber’s value isn’t determined on the ground these days but in the ether, the ‘air beyond the clouds’. Approaching mid-year, the processing industry finally engaged in a little much-needed solidarity – time to ‘do a Bali’ – to wrest back control of its future, a return to control of value based on cost. As paper is no longer a reflection of that value, the decades-old incidence of average-price contracting – once existing contracts have run their course – has gradually been shelved in favour of spot pricing, paper disconnected, its generally declining volumes perhaps indicative of its waning reflection of reality and of the traditional trade’s growing exodus from it. Ditching the average price contract rebalances the supply/demand equation by recovering its bid element, a must for any market if it’s not to be perceived as a ‘seller- only’ one.

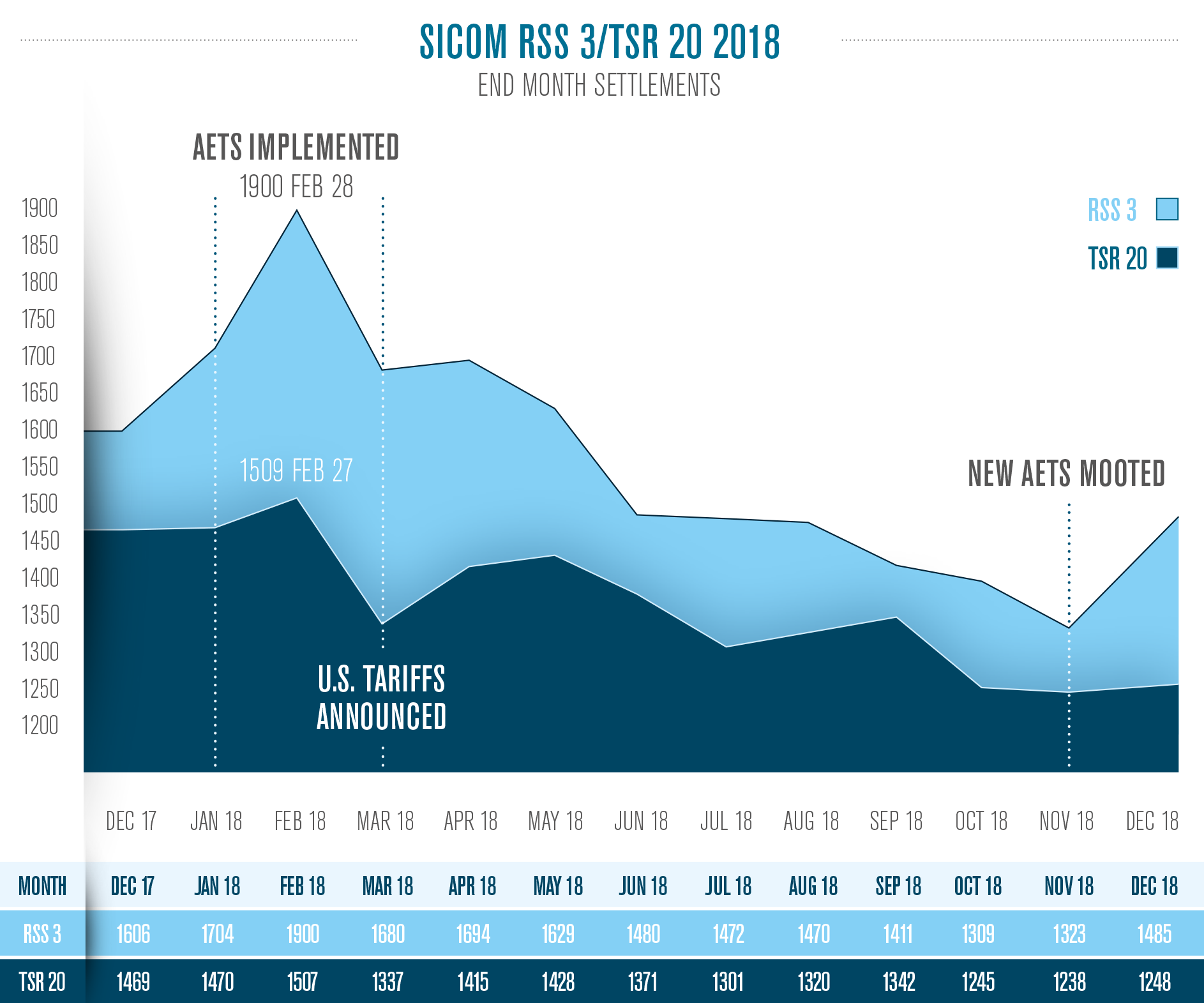

Rubber’s export was ‘limited’ in the first quarter by the Tripartite’s Agreed Export Tonnage Scheme (AETS) but subsequent export numbers for the full year – and substantially lower prices (refer to figure 1, the additional imposition of U.S. tariffs on China didn’t help) – proved the futility of imposing curbs on the natural supply/demand equation. Markets correct themselves far more efficiently when left to their own, time-proven devices. The pity is that, short of any fresh inspiration, the same authority is poised to do it all over again when all that does is to encourage additional and, currently, unwanted output. If it has to be buried in road construction, why produce it in the first place? Serious consideration should, however, be given to proper output control at source, which means re-education and guidance towards alternative income sources to avoid unwieldy and destructive surpluses not, incidentally, limited to rubber.

It’s probably indisputable that since China became the world’s number one importer of natural rubber shortly after the turn of the century, but particularly since it bailed out a bankrupt global financial system following its 2008 debacle, it would become rubber’s main driver and that, whenever it stumbled, the rubber market would do likewise. Inevitably – following the announcement of import tariffs on Chinese goods by President Trump at the end of the year’s first quarter, ostensibly on the back of intellectual property theft that soon turned into a tit-for-tat retaliation, the subsequent deterioration of trade relationships and the parallel imposition by the Chinese government of stricter domestic financial and pollution controls – China’s rubber industry had to suffer, a fact immediately reflected in a ballooning of the Shanghai rubber market’s deliverable stocks, rising by 186,000 mT between the end of 2017 and its reduction – not by consumption but by its validity expiry – in the middle of November, since when it has already replaced 65,000 mT of fresh, certified, but unwanted production. China’s domestic output apart, the wider rubber-producing industry has been slow to adapt to China’s reduced demand as its perceived ‘driver’ languishes in the limbo of the uncertainty it finds itself in, dependent on political face-saving rather than its own ambitions and fundamentals.

China’s industrial statistics at year-end are not encouraging although, given the agreed ‘ceasefire’ on further impositions or tariffs extensions over the first quarter of 2019, and the fact that both sides acknowledge they’re currently seriously talking to each other, should they find common ground and some flexibility, rubber could become positively volatile in no time at all. If one believes in cycles, particularly of the seven-year variety, the next turn is already a year overdue as rubber prices peaked early in 2011.

Towards the end of a troubled year when there was actually little sign of either an immediate surplus at origin or, indeed, of the seasonal peak in production in most of rubber’s producing areas in South East Asia – output actually reported lower in many areas, some due to low price considerations – we might need to question if the still-perceived ‘surplus’ is due to woolly statistics, an ‘inherited’ stock build-up or to a real imbalance in supply and demand that hasn’t yet had due effect on dented sentiment? If Shanghai’s stock of rubber that is no longer popular in usage is removed from the equation, where do we really stand? If inventories are of unwanted product, should they affect the one in demand? Probably not? Most definitely not.

The paper markets have suffered a loss of confidence in terms of being representative of their ‘hosts’. It could be that they have only themselves to blame. The introduction of every new contract tends to dilute the existing ones as traders will always prefer single to multiple price references. Given the stock situation in China and the fact that a previously internationally-respected Technically Specified Rubber (TSR) 20 contract already exists in non-partisan Singapore, did the Shanghai market really need to announce a new arrival? Did Tokyo? What did those announcements, and subsequent flotation of a Standard Thailand Rubber (STR) 20 Free On Board (FOB) contract, do for interest in Japan? Nothing if statistics prove anything. Arbitrage business? Largely for the birds: can anyone effectively arbitrage, or feel safe in doing so, where one leg of the structure is largely nominal and difficult to exit at will? But back to Rubber 2018. The announcement or threat of an AETS imposition gave the rubber market a false, short-term boost. On January’s implementation of the scheme, Ribbed Smoke Sheets (RSS) 3 prices rose by almost $300/tonne, TSR20 by a modest $40 by the end of February, signaling that the only real beneficiary was Thailand, which subsequent statistics showed as having ‘suffered’ little export reduction, if any at all. The penalty for arm twisting the market was obvious in the following decline that saw no meaningful arrest until December’s revival on the potential of a new AETS. Starting at an already low point, where can that possibly lead? Surely to just another repeat, yet another defeat (refer to figure 1), particularly when viewed against a background of global economic disorder. A tightening of European emissions standards, brewing since the ‘Diesel-gate’ scandals, scored an additional own goal as far as second-half European auto sales figures were concerned, China’s also declining as earlier tax advantages expired and the trade war impacted on both sentiment and spending. The only economic beacon still shining, the U.S., just kept its head above water.

At the end of 2018, we find ourselves in the middle of a finely-balanced quandary: will rubber’s real fundamentals overcome its external obstacles? They should, if self-determination wins the day, but if rubber-specific Quantitative Easing (QE) is applied, again, they might not. A quick fix is just that. Quick, and short. We don’t need to be ‘Tripartite-ed’ again. In the meantime, with global climate patterns both changing and surprising, often with extremes, it’s beginning to look like an end-year without a defined peak production period. Should that confirm itself over the next few weeks, there may well be cause for rubber optimism and, if the U.S. Federal Reserve is really done with interest hikes for the time being, a weaker dollar could well translate into price support for commodities, including ours.

After what can only be described as a bad year, there appears to be a convergence of positives in the rubber market that signals better days ahead. In the middle of December, we ran a poll asking correspondents where they thought the market would be at the end of March 2019. There was an overwhelming lack of bearish sentiment, 8:1 respondents seeing an improvement in value over the course of the first quarter. Time and sentiment will tell. We’re a China-centric industry so, to end on a light note, we’ll turn to the Zodiac and the Year of the (Earth) Pig: Pigs generally have smooth prospects for the coming year…their wealth will increase…it’s a good year for entrepreneurs to develop their businesses…pigs will have very good financial prospects in 2019…will do well in their investments and be well rewarded. What more can we ask?

______________________________________

George Sulkowski

Chief Economist, Corrie MacColl