Voluntary Business Updates (Q1 2021)

SINGAPORE, 17 May 2021 – Halcyon Agri Corporation Limited (“Halcyon Agri”, the “公司名称” and together with its subsidiaries, the “Group”), announces operating and financial performance for the first quarter ended 31 March 2021 (“Q1 2021”).

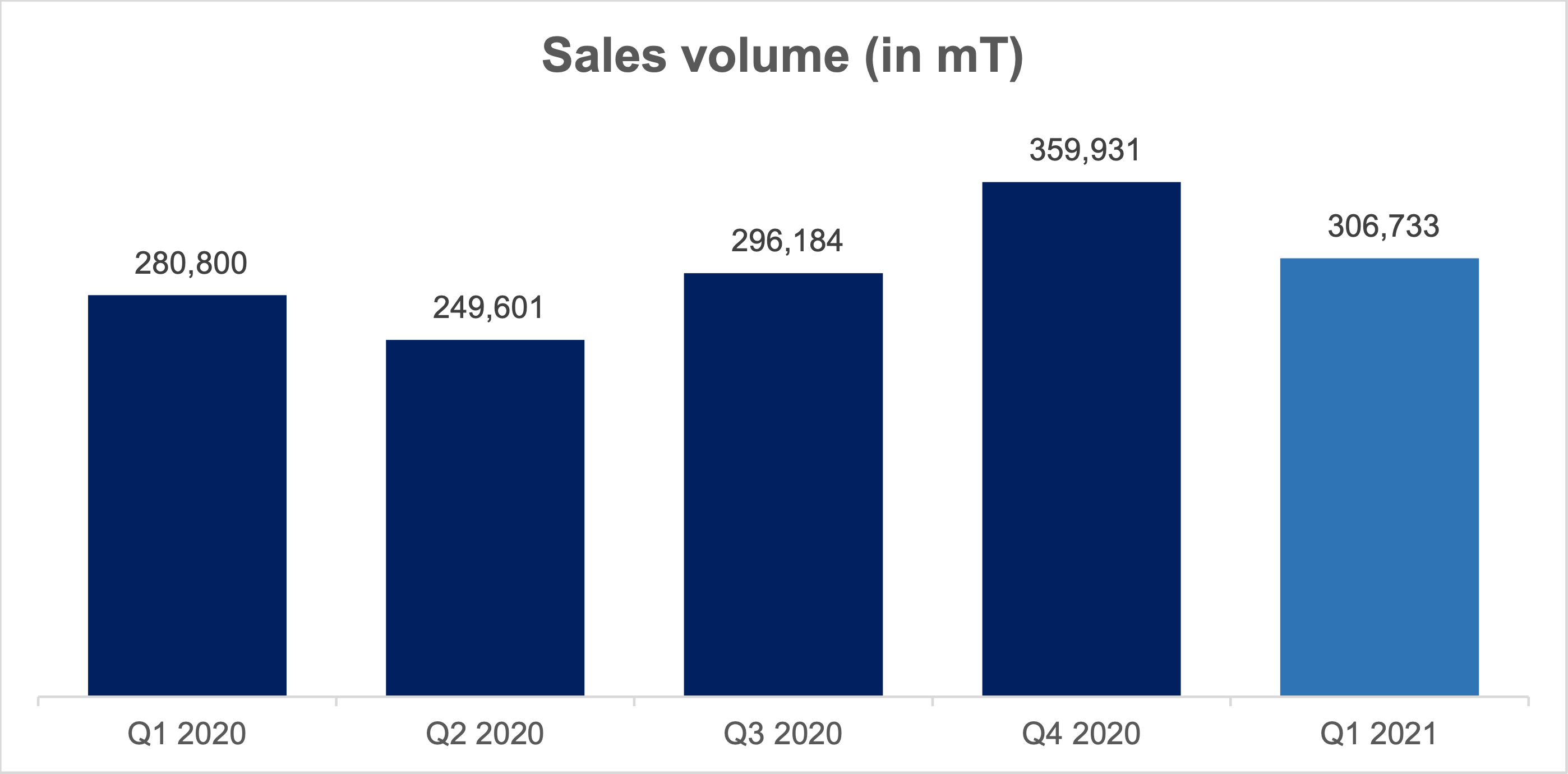

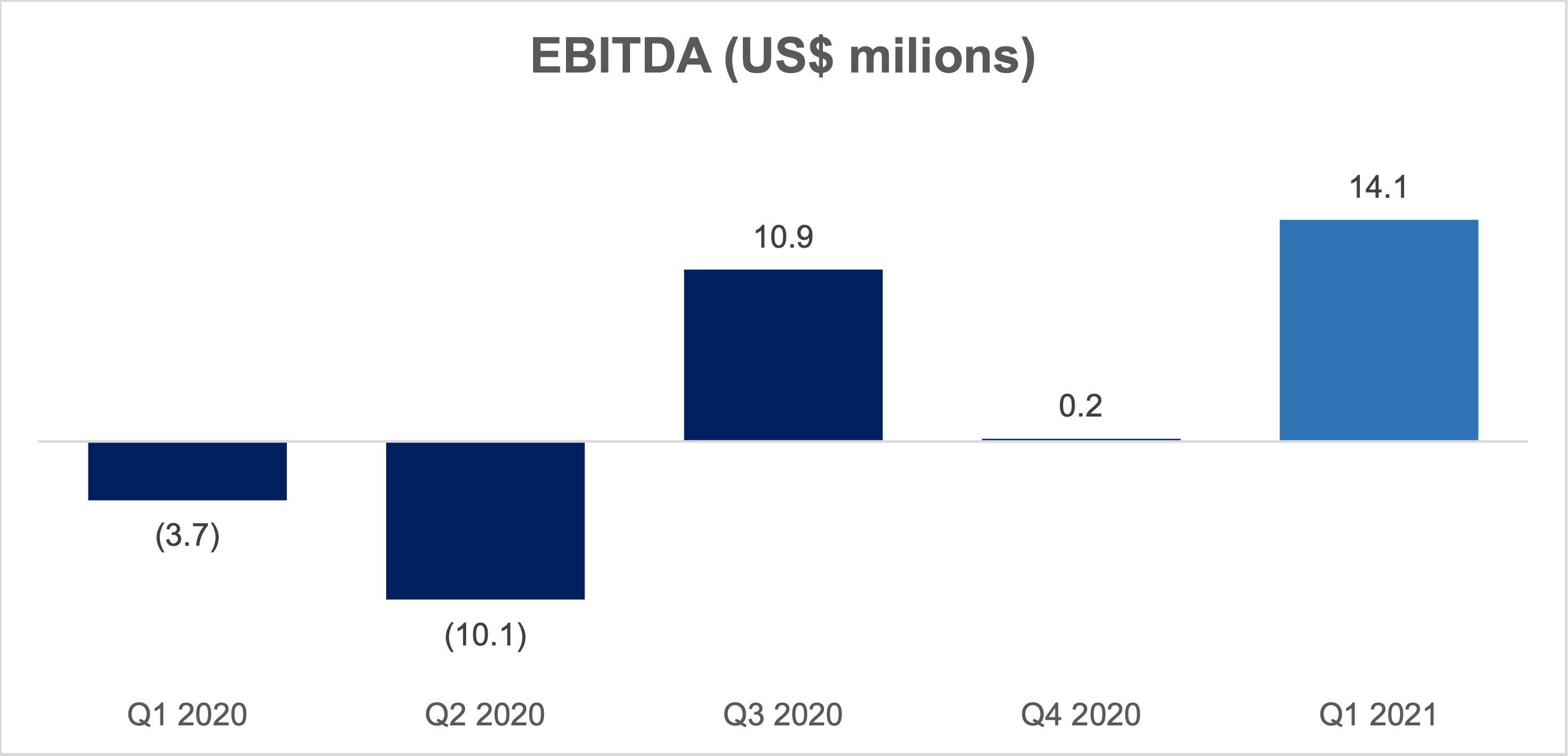

The Group witnessed robust demand for natural rubber that underpins the uptrend in natural rubber prices during Q1 2021. Sales volume in the first quarter was 306,733 mT, 9.2% higher than Q1 2020. Driven by margin expansion and effective cost control, the Group has reported a Q1 2021 EBITDA of US$14.1 million – outperforming Q4 2020 and Q1 2020 EBITDA of US$0.2 million and negative US$3.7 million respectively. Coupled with the reduction in net financing costs, the Group has achieved a profit before tax position in Q1 2021.

Commenting on the Group’s improved financial results, Mr Li Xuetao, Chief Executive Officer of Halcyon Agri said, “Since Q2 2020, we have made remarkable progress in all aspects of our business. The Q1 2021 financial results is a testament of this progress. On the back of the improving market sentiments, we are confident that the Group is heading towards the right direction. Our integrated global supply chain has given us the opportunity to continue staying close to our customers in meeting their increased demands and requirements.”

“The rubber market remains upbeat and Halcyon Agri, having strengthened its balance sheet through recent completion of several financing initiatives, is well-positioned to ride on market recovery for further growth and to continue creating value for our stakeholders.”

During this quarter, Halcyon Agri has also accomplished several milestones which included:

(i) | Secured a three-year syndicated term loan of up to US$300 million. Funded by a syndicate of banks, the facility strengthened the Group’s liquidity and financial reserve. |

(ii) | SGX’s¹ investment in HeveaConnect, with Halcyon Agri ceding its controlling stake in advocating for a fair and independent marketplace. With the completion of these initiatives, HeveaConnect would be able to move into its next phase of growth by onboarding more producers and tyre makers onto the platform, in supporting the development of a fair and independent marketplace for sustainable natural rubber. HeveaConnect will now be accounted for as an associate of the Group, with a gain on dilution² of approximately US$4 million recorded. |

(iii) | Ranked the most transparent rubber producing company globally under SPOTT³ assessment. This adds to the expanding list of accolades recently obtained by the Group, and exemplifies recognition by respected third-party organisations and demonstrates our commitment to high sustainability standards. |

In addition, Halcyon Agri will continue to focus on optimising its capital structure and unlocking value through opportunistically divesting its non-core assets.

Industry trends and outlook

Source: Bloomberg

Natural rubber prices (indicated by SICOM TSR20 1st position) closed at US$1,662 per MT in the first quarter of 2021 following a pullback from a four-year high of US$2,000 per MT in end-February 2021. Prices were supported by pent-up demand post-lockdowns and tightened supply due to early-wintering and above-normal rainfall in Southeast Asia, a key rubber producing region, during Q1 2021. Q1 2021 closing price represents an increase of 10.6% and 60.1% over Q4 2020 and Q1 2020 closing prices, respectively.

Global economic recovery remains strong, as shown by recent gross domestic product (GDP) growth numbers from the US and China, two of the world’s largest economies. Similar sentiment was echoed by the International Monetary Fund (IMF), which increased its global growth projections for 2021 and 2022 to 6% and 4.4% (previously 5.5% and 4.2%) respectively.

While global recovery gathers strength, the global shortage of shipping containers has caused enormous strain on the international supply chains. Such a situation has disrupted global trade, hindering the movement of natural rubber cargoes from Asia to Europe and the US. This had a domino effect down the supply chain, where the customers that procured rubber from Asia are hampered with shipment delays, or suffered higher freight costs.

The Group believes that these developments will provide further tailwinds for natural rubber demand and prices in near-to-middle term. As an integrated global supply chain manager for natural rubber, Halcyon Agri is well-positioned to leverage its strong presence in major rubber- producing regions and its extensive global distribution network to source, process and distribute its rubber products internationally.

Commenting on his expectations of the industry, Mr Li said, “Like a rubber ball that bounches back, natural rubber prices has risen sharply in the past months and is well above its pre-pandemic peak in February 2020. This is reflective of our earlier expectations of an increasingly robust downstream demand as the global economy reopens. However, the global pandemic situation remains fluid. Recent emergence of new strains and new wave of outbreaks have shown that the pandemic is far from over, and the growth trajectory of global economy that we have been seeing may potentially be disrupted.”

“Notwithstanding this, we continue to see stable and improving stream of offtakes from our customers and the downstream factories are operating at full speed. This goes to show that near- term demand outlook is looking positive. However, considering the fluid situation of the pandemic and that massive lockdowns remain possible, we are cautiously optimistic on the long-term prospects for natural rubber.” Mr Li added.

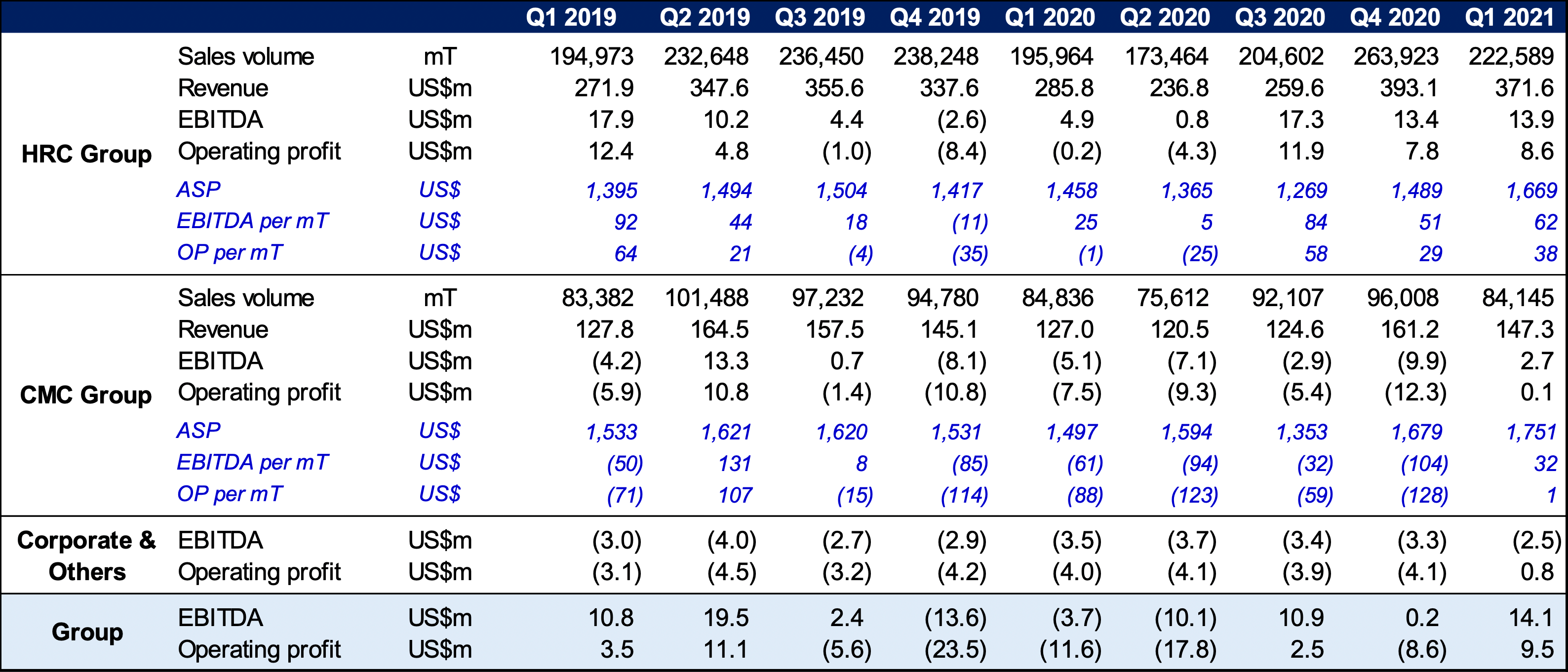

Key Q1 2021 financial performance summary

Financial performance

During the quarter under review, sales volume increased by 9.2% from Q1 2020, reflecting the favourable market condition now as compared to Q1 2020 which was affected by COVID-19 pandemic, 14.8% lower than Q4 2020, despite a stronger order backlog, was mainly due to the pent-up demand from most customers in H2 2020 following the progressive lifting of lockdown restrictions. While the current disruptions in global logistics have affected some of our fulfilment to customers, we have been managing this situation closely with our customers. Any incremental costs were passed on further downstream.

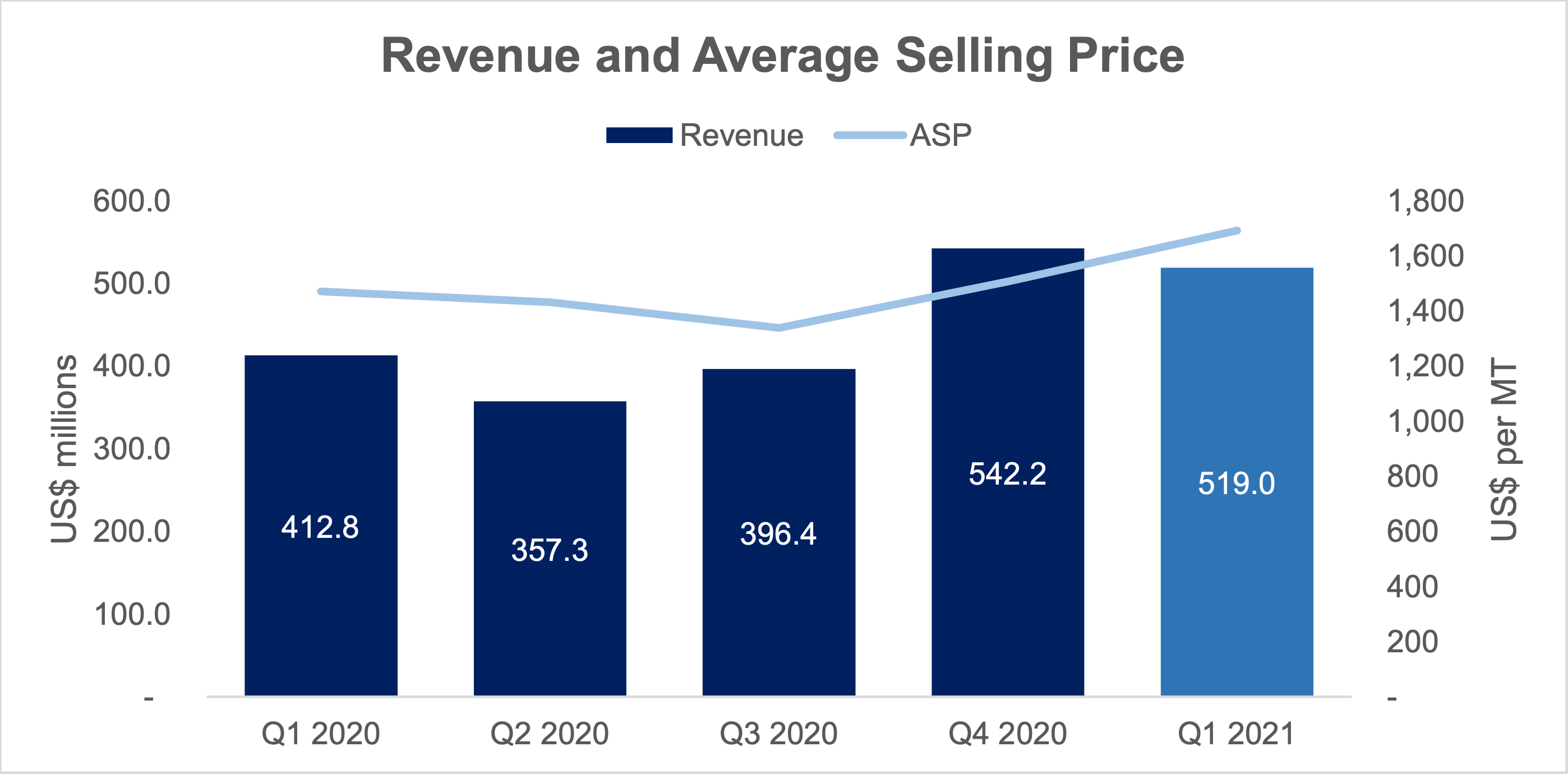

Q1 2021 revenue of US$519.0 million represents a 25.7% increase from Q1 2020, but a 4.2% reduction as compared to Q4 2020, which is in line with sales volume trends. Notwithstanding, the average selling price (ASP) has trended upwards alongside the rubber prices.

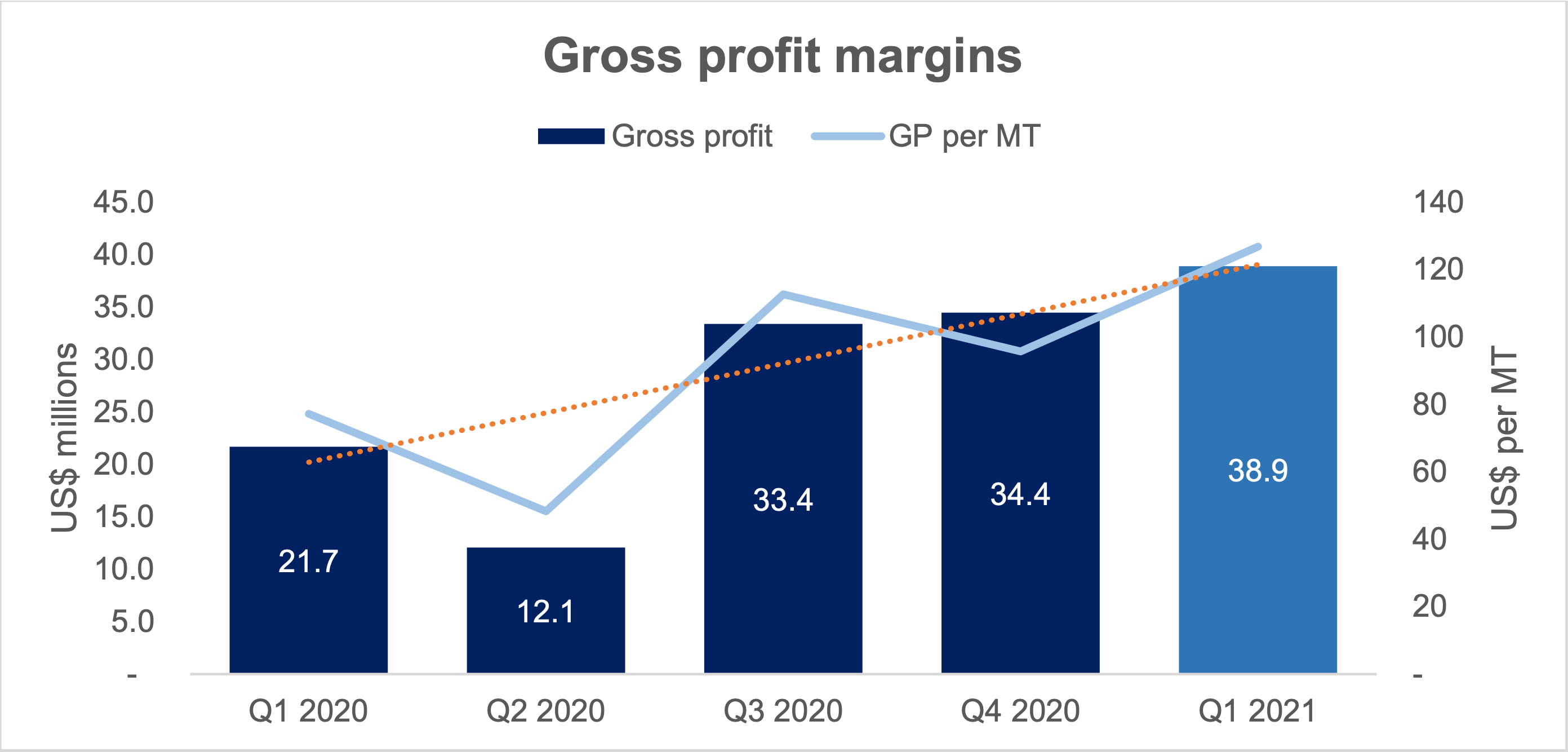

The Group recorded higher gross profits, from US$34.4 million in Q4 2020 and US$21.7 million in Q1 2020, to US$38.9 million in Q1 2021. The Group’s continued focus on margin optimisation, and deploying agile supply chain strategies had resulted in consecutive quarters of gross profit expansion. Gross profit per mT was US$127 in Q1 2021, 23.3% and 32.3% higher than Q1 2020 and Q4 2020 respectively.

Note: EBITDA, as defined herein, excludes fair value gains on biological assets and investment properties in the respective periods.

EBITDA increased significantly in Q1 2021 to US$14.1 million when compared to both Q1 2020 and Q4 2020, largely driven by strong margins and effective cost control measures.

Segment overview

HRC Group

Revenue increased by 30% from US$285.8 million in Q1 2020 to US$371.6 million in Q1 2021, which was equally contributed by an increase in volume and a higher ASP. Gross profits up by 44.9% from Q1 2020’s US$17.8 million to US$25.8 million in Q1 2021. HRC Group continues to differentiate itself as the premium producer of tyre-grade rubber from desired origins and the improvement in results reflect the effectiveness of our margin optimisation strategies.

CMC Group

Buoyed by higher ASP, revenue rose by 15% from US$127.6 million in Q1 2020 to US$147.3 million in Q1 2021. Gross profit more than doubled from US$3.9 million to US$13.1 million over the corresponding period, which is attributable to CMC Group’s strong presence in Europe and the US. Its ability to offer just in time deliveries relieves the acute domestic shortages, which allowed them to command a substantial sales premium. The downstream distribution margins are more than sufficient to cover the maintenance costs of upstream plantations.

Please refer Appendix for a summary of operating statistics.

Appendix – Selected operating statistics summary

Note: The EBITDA and operating profit figures above excludes fair value gains on biological assets and investment properties in the respective periods.